The $110 Billion Buffer

How the Philippines Built a Fortress Economy While the Rest of the World Was Distracted

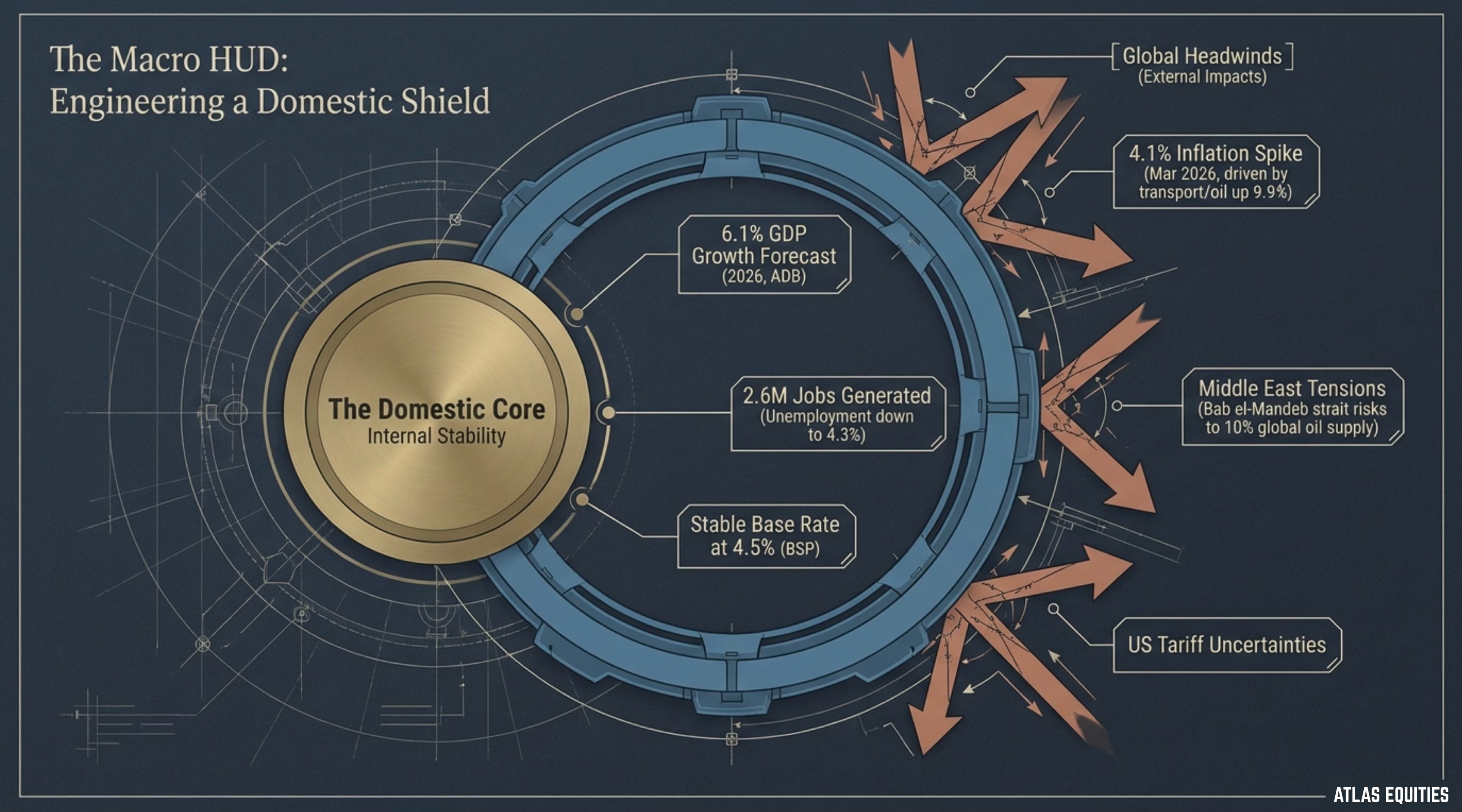

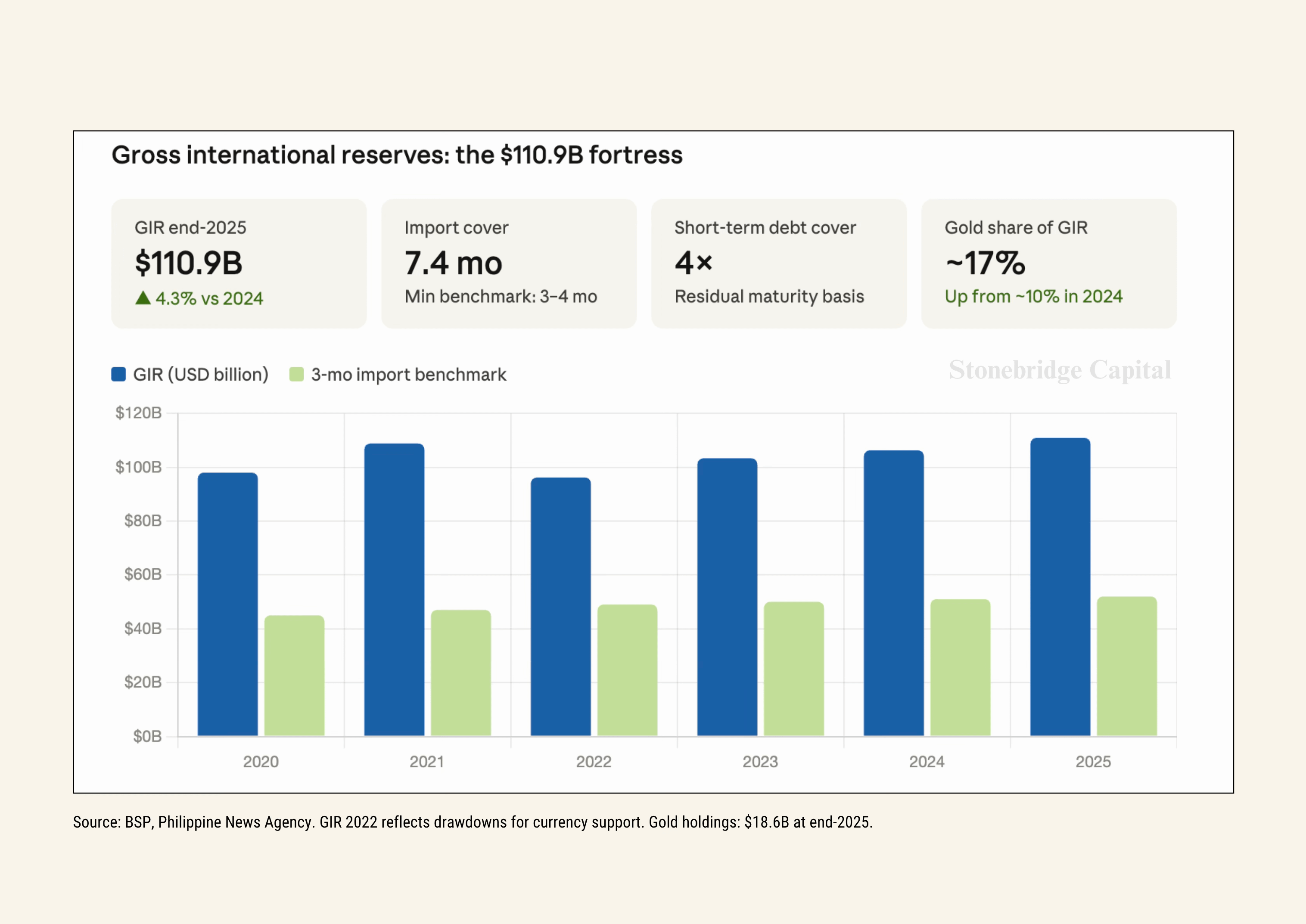

There is something quietly remarkable happening in the Philippine economy that most international observers have not fully appreciated. On the surface, the numbers look worrisome. In March 2026, the Philippine Peso touched an all-time low of PHP 60.55 against the US dollar, the kind of figure that typically precedes a currency crisis, a sovereign debt panic, or at minimum a sharp downgrade in investor confidence. And yet, at the exact same moment, the country was sitting on US$110.9 billion in gross international reserves, a record high not seen in decades. These two facts, held together, define something more interesting than either one alone: a country that has quietly built one of the most resilient economic foundations in Southeast Asia, even as the peso chart tells a different story.

Understanding this paradox is the starting point for understanding why the Philippines deserves more serious attention than it typically receives.

If you’d like to support our work, you can send a tip via PayPal. Every bit helps keep things running!

The War Chest

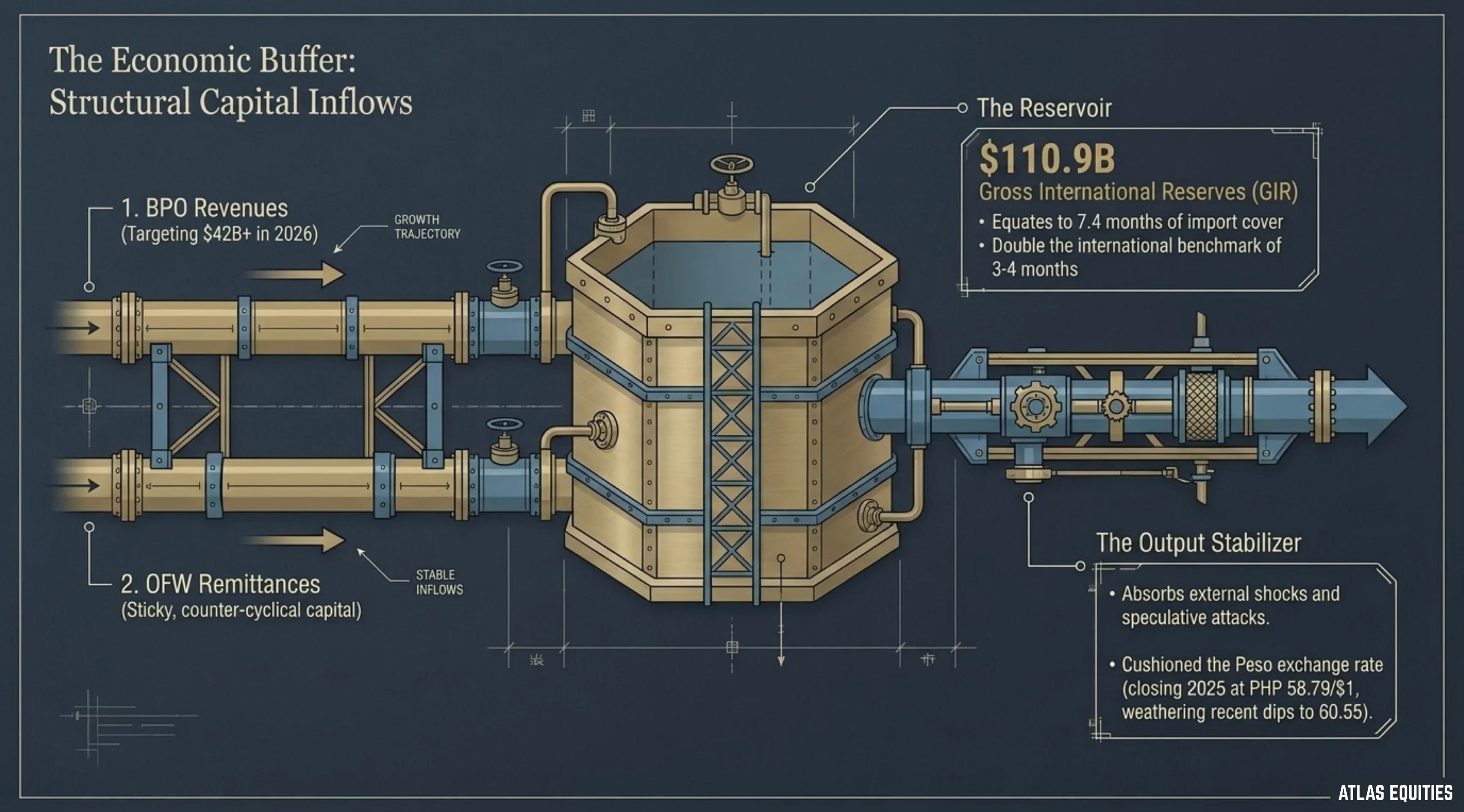

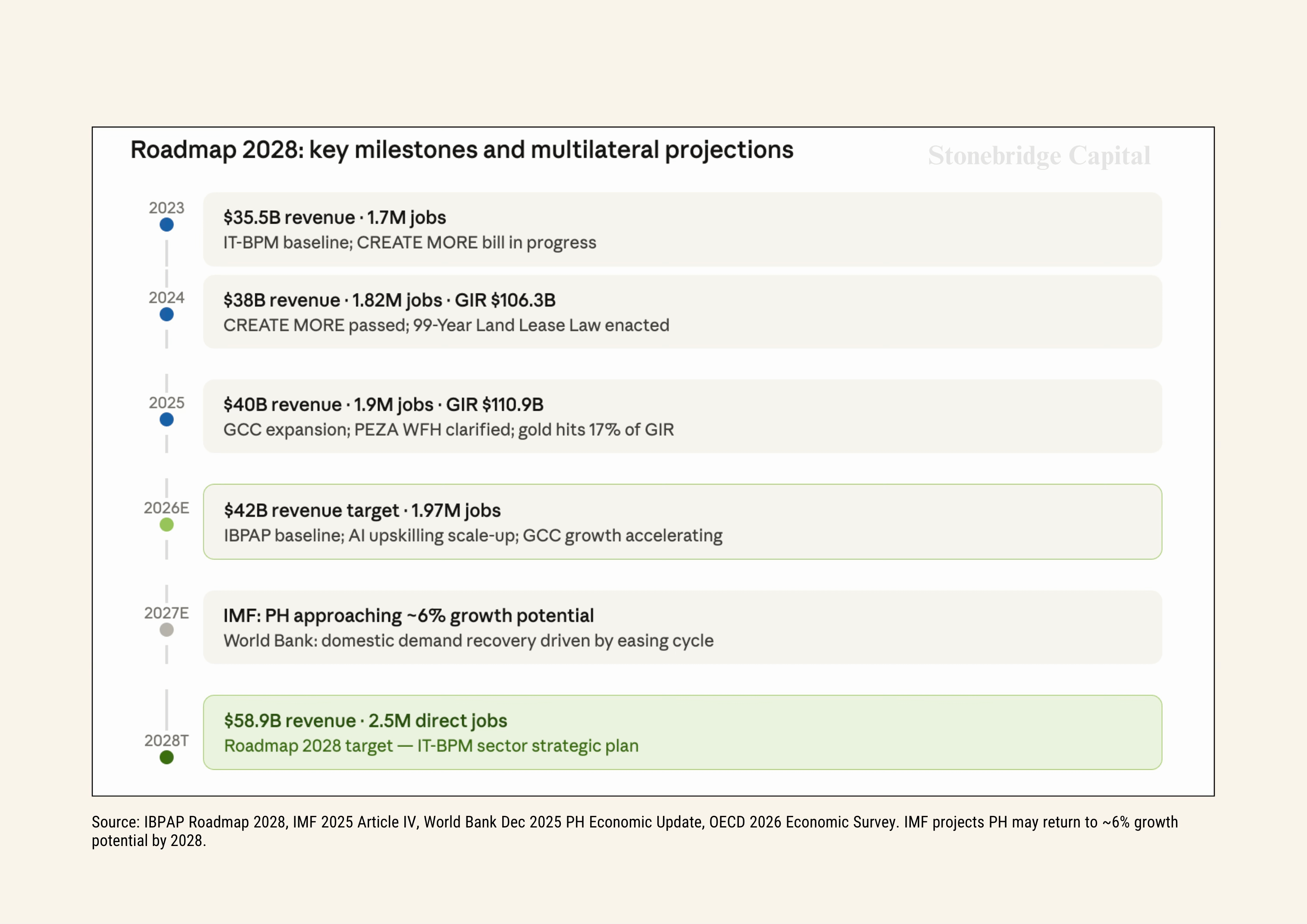

The Bangko Sentral ng Pilipinas reported that by end-2025, Gross International Reserves had climbed to US$110.9 billion, up from US$106.3 billion the year prior. To put this in practical terms, the BSP notes that this stockpile covers 7.4 months’ worth of imports, nearly double the international benchmark of three to four months that economists use as a minimum threshold for reserve adequacy.

These reserves are not merely a statistical achievement. They are a functioning defense mechanism. Composed of gold, foreign exchange holdings, and foreign-denominated securities, they represent the country’s capacity to finance essential imports and service its external debt obligations even during periods of severe market dislocation. When currency speculators probe for weakness, a reserve buffer of this magnitude is what keeps a central bank credibly in the fight.

RCBC Chief Economist Michael Ricafort framed it plainly:

“Still relatively high GIR compared to recent years and decades, now at USD110.9 billion, could fundamentally provide some support, buffer, and cushion for the peso exchange rate, especially versus any speculative attacks, amid proceeds of foreign borrowings and funding requirements by the government and by the largest companies.”

The peso may be weak, in other words, but the Philippines is not. That distinction matters enormously when assessing where the economy goes from here. The multilateral community has been equally direct in its assessment. ADB Country Director for the Philippines Andrew Jeffries put it in terms that carry real institutional weight:

“The Philippines’ growth outlook remains resilient amid a global environment of shifting trade and investment policies and heightened geopolitical uncertainties. Though these uncertainties pose increased risk, we see strong domestic demand anchoring growth, with sustained investments and an accommodative monetary policy supporting the economy’s expansion.”

This is not the cautious, hedged language that multilateral institutions typically deploy when they are quietly worried. It is a genuine statement of confidence in structural foundations.

The JPMorgan Verdict

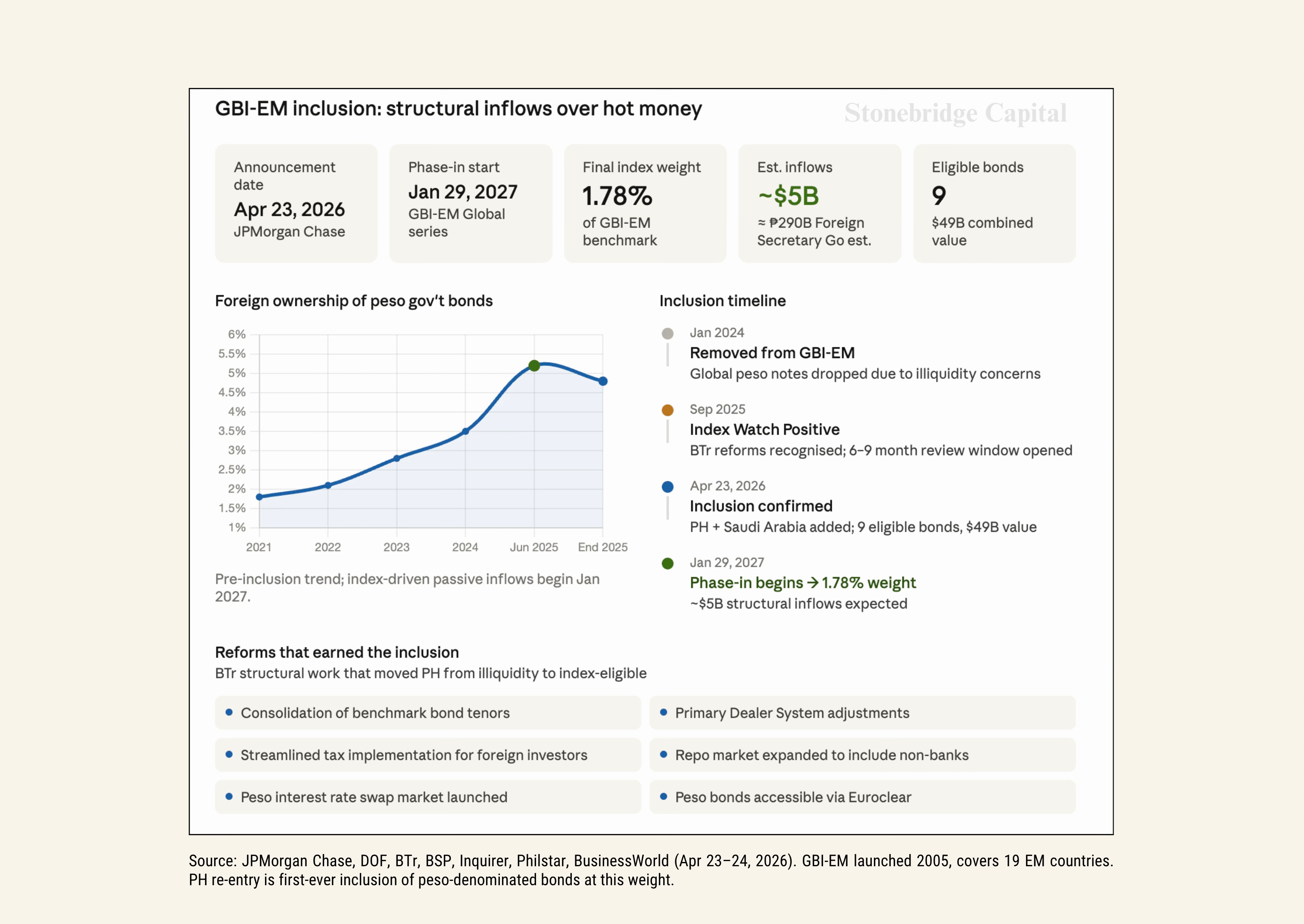

If the reserve buffer is the Philippines’ defensive credential, the JPMorgan announcement of April 23, 2026 is its offensive one. In a development that received significant attention in global debt markets, JPMorgan Chase announced it will add local-currency bonds from the Philippines into its widely followed Government Bond Index-Emerging Markets, or GBI-EM, with the phase-in beginning January 29, 2027, until Philippine bonds reach a final weighting of 1.78% in the benchmark.

To understand why this matters, it helps to understand what the GBI-EM actually is. Launched in 2005 and closely tracked by global fund managers, the GBI-EM covers 19 countries and serves as a key benchmark for local-currency sovereign debt. When a country enters this index, passive funds that mirror its composition are effectively required to buy that country’s bonds. It is not discretionary allocation driven by an analyst’s conviction. It is structural, automatic, and sustained. Nine eligible Philippine government bonds, worth about $49 billion, will officially enter the index on January 29, 2027, and Finance Secretary Frederick Go has estimated that the full phase-in could bring approximately $5 billion in foreign inflows to the local debt market.

The significance of this inclusion extends beyond the capital flows. Philippine peso-denominated government bonds were placed on JPMorgan’s watch list for possible inclusion as early as September 2025, with the Bureau of the Treasury noting at the time that the watch-list placement reflected reforms aimed at improving market liquidity and accessibility. Those reforms included the consolidation of benchmark tenors, adjustments to the Primary Dealer System, streamlined tax implementation, expansion of the government securities repo market to include non-banks, and the launch of the peso interest rate swap market. The JPMorgan inclusion, in other words, is not a gift. It is a grade. The Philippines earned it by doing the structural work that global debt markets actually require.

Finance Secretary Frederick Go made the point directly:

“We welcome the Philippines’ first-ever inclusion in the JPMorgan Government Bond Index for our peso-denominated government bonds. It reflects a strong vote of confidence in our solid fundamentals and fiscal discipline. This milestone will broaden our investor base, improve market liquidity, and help lower borrowing costs.”

BSP Governor Eli Remolona was equally direct about what the inclusion means for the broader capital markets ecosystem:

“This is a major step in deepening the Philippine capital markets, with significant benefits to the government, to domestic and global investors and to local banks and businesses. As bonds gain more liquidity, this will help the BSP transmit monetary policy, benefiting borrowers and investors across the economy.”

The private sector read the signal in similar terms. Jonathan Ravelas, Senior Adviser at Reyes Tacandong and Co., offered an assessment that cuts to the core of what index inclusion actually does for a sovereign debt market:

“The Philippines’ inclusion in the JPMorgan Government Bond Index is a major credibility upgrade. It effectively puts Philippine bonds on the ‘must-own’ list for global investors, driving steady, long-term foreign inflows rather than hot money.”

That last phrase deserves emphasis. The distinction between structural inflows driven by index inclusion and “hot money” driven by short-term yield chasing is not semantic. Hot money amplifies volatility. Index-driven inflows compress risk premiums over time and deepen market liquidity in ways that benefit every borrower in the economy, from the national government down to the household taking out a mortgage. The Philippines has just secured a source of the former, at a moment when the peso could use exactly that kind of durable external anchor.

From Cost Arbitrage to Strategic Intelligence

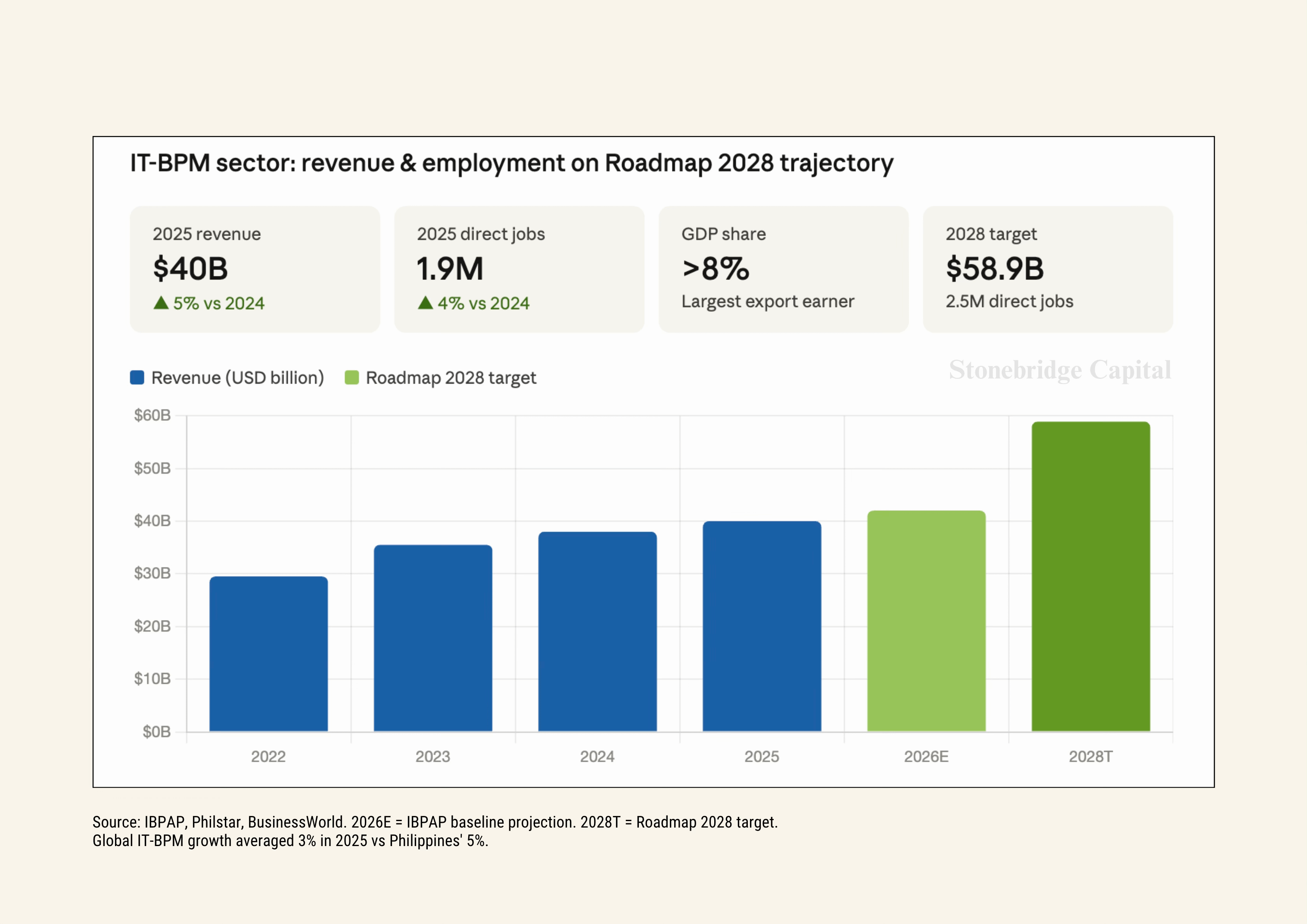

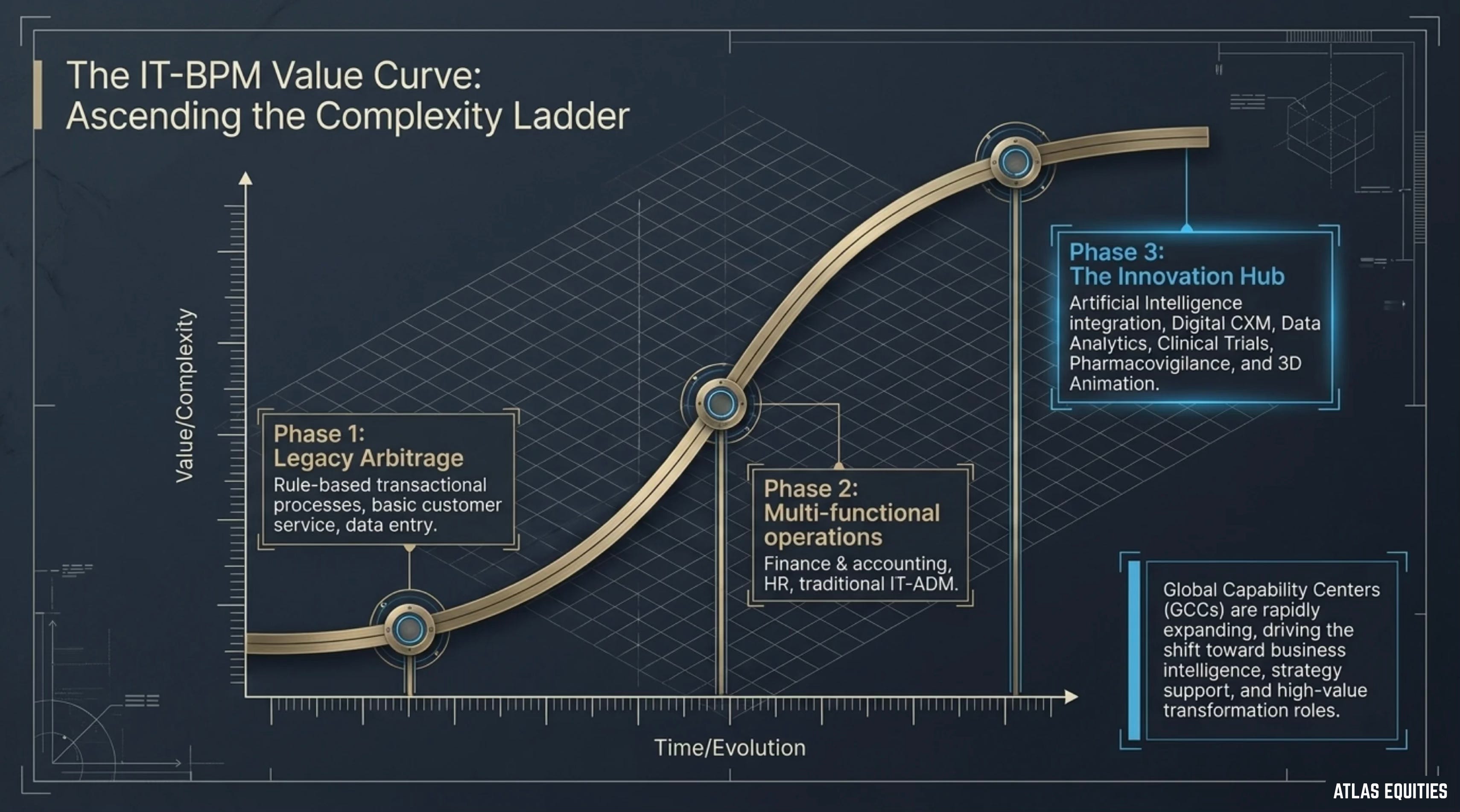

The reserves story is compelling on its own, but it becomes even more significant when you understand what is driving the underlying economic engine. For the better part of three decades, the Philippines built its services sector on a straightforward value proposition: it offered English-speaking, technically capable labor at a fraction of what similar work would cost in the United States or Europe. That model worked. It created millions of jobs, generated billions in export revenue, and turned Metro Manila into one of the world’s most recognizable outsourcing destinations.

But the industry’s own roadmap acknowledges a hard truth. What worked to get here will not be sufficient to take the country where it needs to go next.

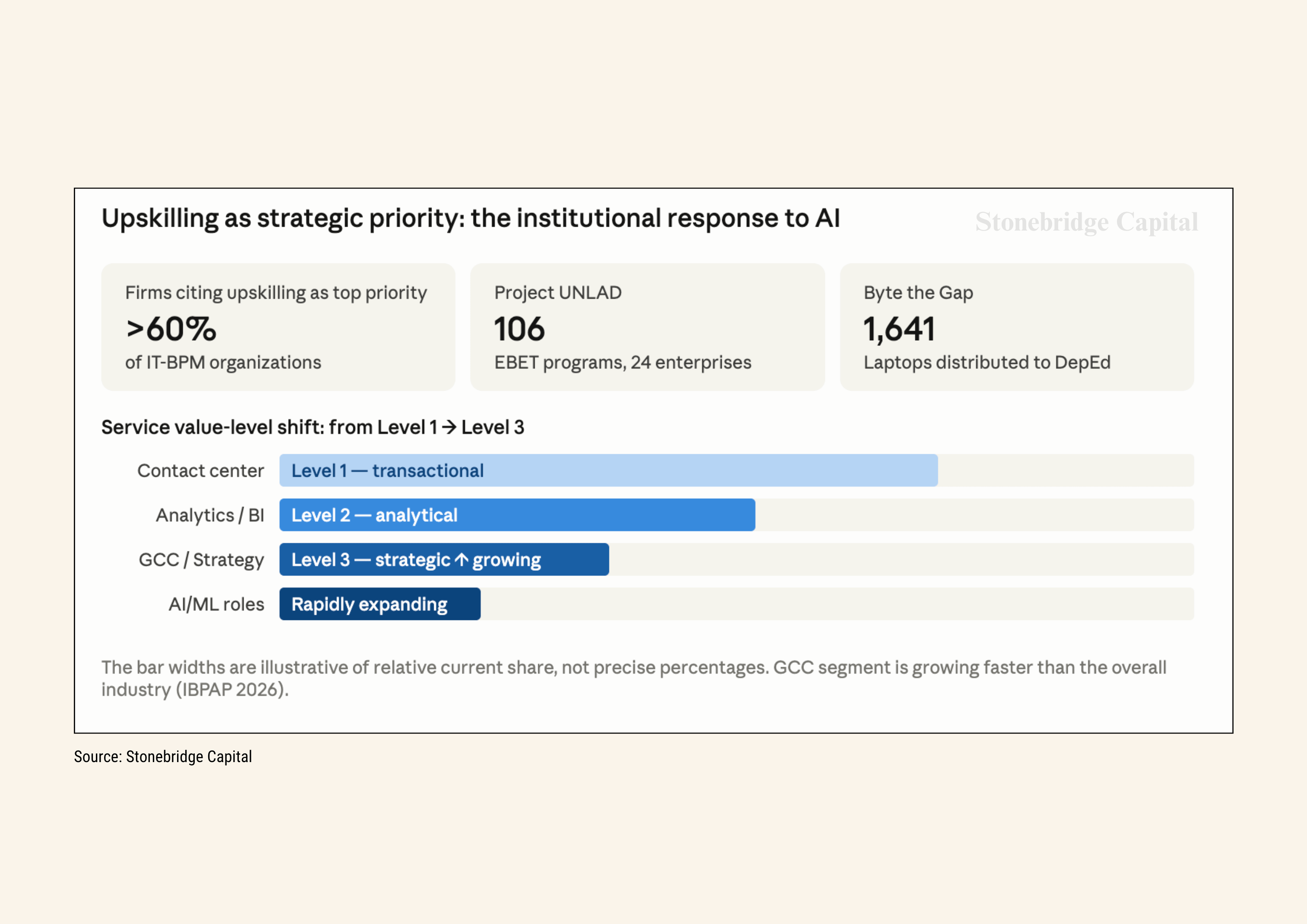

The IT-BPM sector, now operating under what the industry calls “Roadmap 2028,” is executing a deliberate pivot away from Level 1 transactional work toward what practitioners describe as Level 3 value-added and strategic work. The terminology matters less than the substance: Filipino professionals are increasingly being deployed in Business Intelligence and Data Analytics, Cloud Operations and Cybersecurity, Transformation Strategy and Project Management, and Artificial Intelligence and Machine Learning roles. These are not call center functions dressed up in new language. They represent a genuine structural upgrade in the type of economic activity the country is competing for.

The visible expression of this shift is the rapid expansion of Global Capability Centers, or GCCs, which are dedicated offshore hubs where multinational companies house increasingly sophisticated internal functions. The Philippines is emerging as a preferred location for GCCs focused on customer experience and healthcare services, two sectors where the combination of language proficiency, cultural alignment with Western markets, and improving technical capability creates a durable competitive advantage.

IBPAP President Jack Madrid has been direct about the stakes involved:

“What got us here will not be enough to take us where we need to go next. Our focus moving into 2026: relentlessly upskill our workforce, embrace higher-value work, and continue working closely with government, academe, and investors to keep the Philippines at the heart of global services.”

This is not the language of an industry coasting on legacy advantages. It is the language of an industry that understands its window for transformation is finite. The OECD’s 2026 Economic Survey of the Philippines offers important context for why this transformation matters beyond the IT-BPM sector alone. The organization noted:

“The Philippines is among the world’s fastest-growing emerging market economies, with output more than doubling since 2010 while poverty has halved. A dynamic modern services sector, especially in business process outsourcing, continues to drive performance.”

But the same report was clear-eyed about what comes next. Maintaining that trajectory, the OECD argued, requires a decisive shift toward structural reforms that foster competition, deepen investment openness, and improve governance. The foundation is real. The next phase demands execution that the previous phase did not.

The Geography of Growth

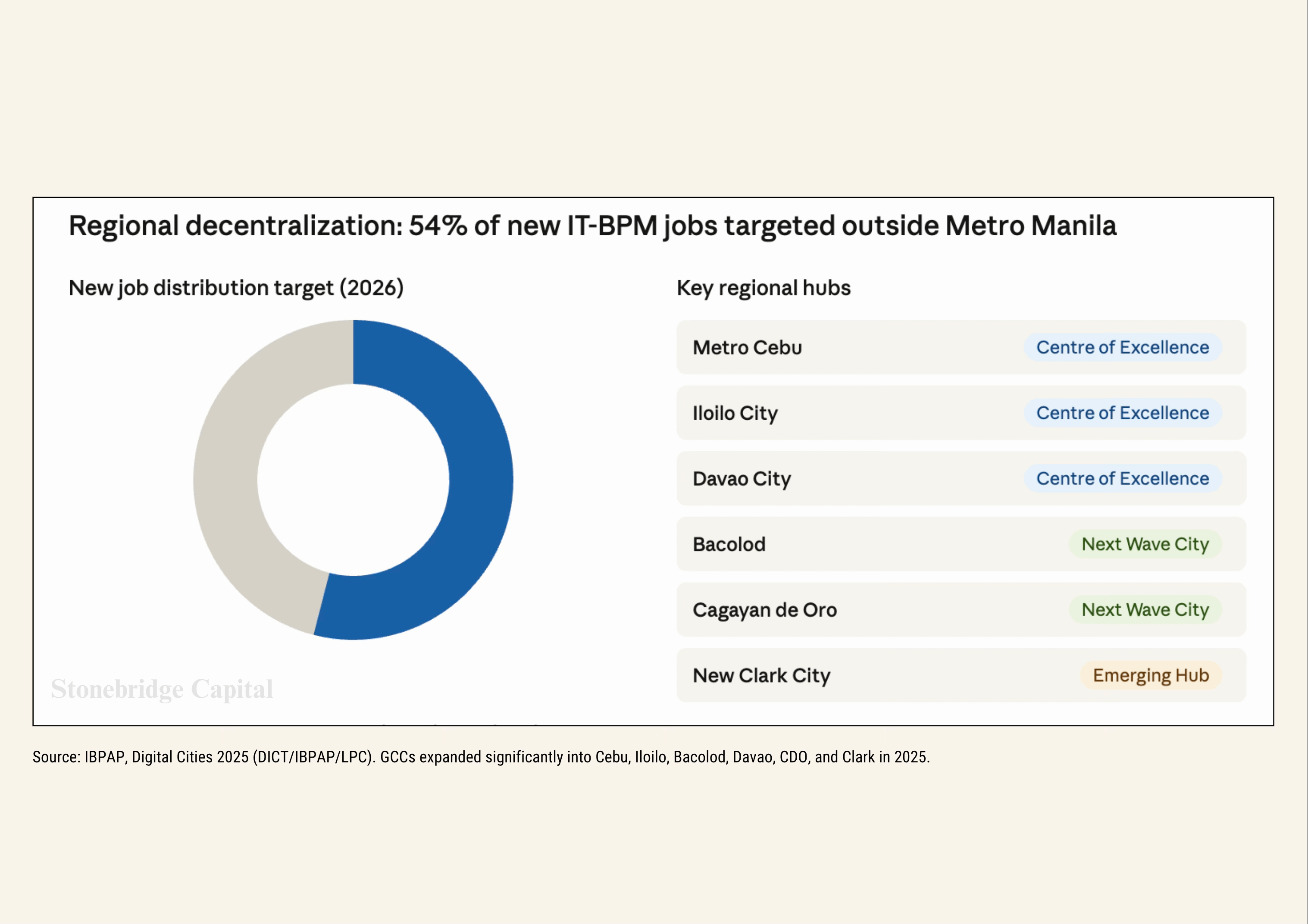

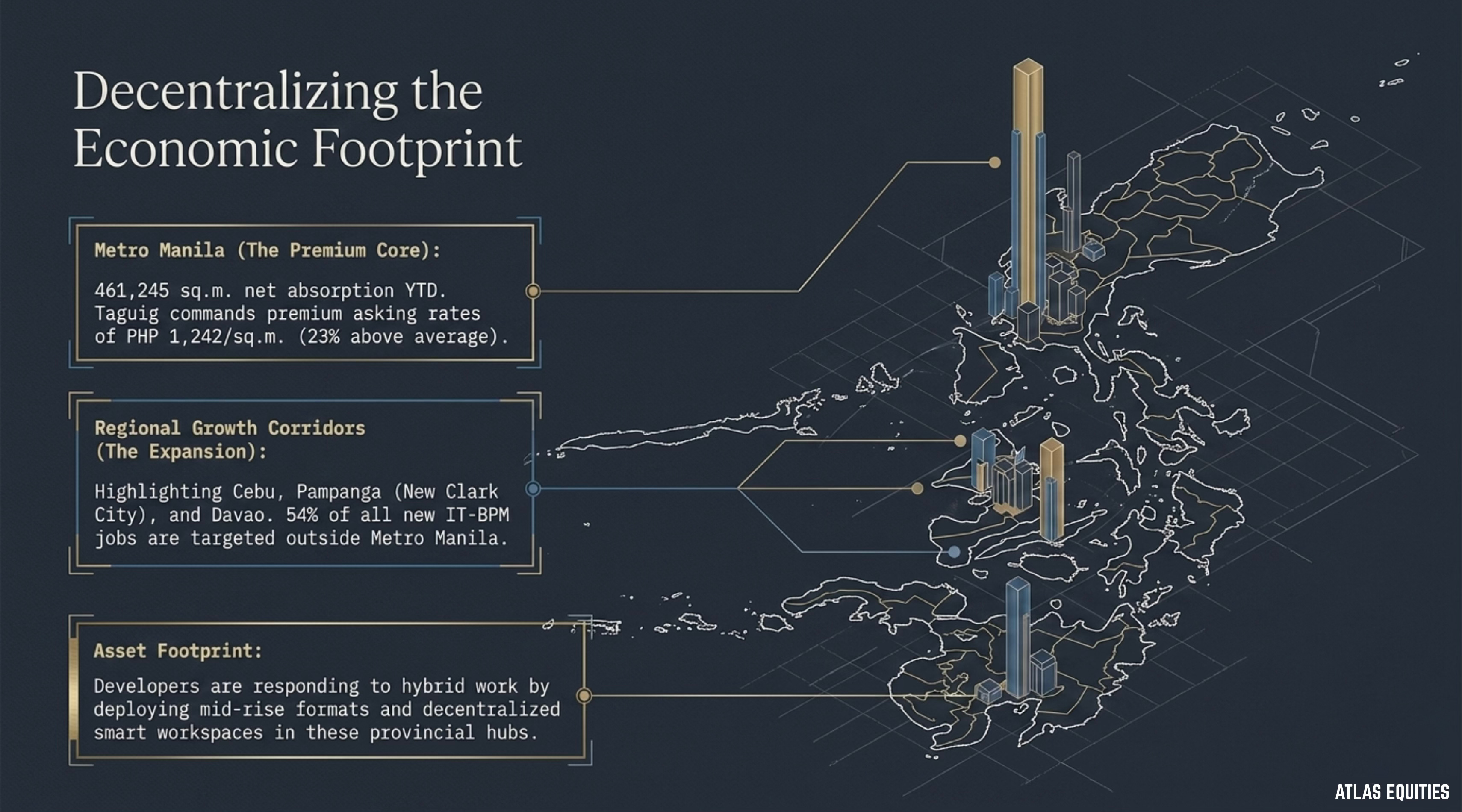

One of the more underappreciated dimensions of the current expansion is its geographic spread. For most of its history, the Philippine IT-BPM industry was effectively a Metro Manila story. Makati, BGC, and Ortigas absorbed the bulk of office investment, talent concentration, and economic activity. The provinces watched from a distance.

That pattern is changing, and the numbers are significant. In 2026, 54% of new IT-BPM jobs are targeted for locations outside Metro Manila. Regional cities including Cebu, Iloilo, Bacolod, Davao, Pampanga, Cagayan de Oro, and the emerging New Clark City are being positioned as what the industry calls “Next Wave Cities,” alternative delivery hubs that offer global firms lower operating costs, deeper untapped talent pools, and opportunities for what the sector describes as “Impact Sourcing,” essentially job creation in communities that have historically been bypassed by the outsourcing boom.

The infrastructure investment underpinning this decentralization is real. The Malolos-Clark Railway Project is improving connectivity across the Luzon region in ways that make provincial operations increasingly bankable for international investors. When infrastructure catches up with ambition, the economics of regional expansion improve rapidly, and the Philippines appears to be crossing that threshold.

This geographic expansion connects to a broader investment thesis that the World Bank articulated in its December 2025 Philippines Economic Update. World Bank Division Director for the Philippines Zafer Mustafaoğlu was pointed in his assessment:

“The Philippines can leverage its strong economic foundations to implement bolder reforms that can unlock faster, more inclusive growth. Removing barriers that limit investment and productivity and strengthening competitiveness can create more and better-paying jobs, expand opportunities, and reinforce economic resilience.”

The decentralization of the IT-BPM sector is, in practice, exactly the kind of inclusive growth mechanism that institutions like the World Bank have been urging the country to develop.

AI as Accelerant, Not Threat

The conventional narrative around artificial intelligence and services-sector employment is straightforward and mostly gloomy: automation will hollow out the kind of repetitive, process-driven work that outsourcing centers depend on, and countries like the Philippines will suffer disproportionately. This narrative is not entirely wrong, but it is considerably less than the full picture.

Within the Philippine IT-BPM industry, AI is functioning more as an accelerant of the strategic pivot than as a direct threat to employment. More than 60% of IT-BPM organizations now cite workforce upskilling as their top strategic priority, which is a telling signal. Rather than managing a workforce reduction, these companies are investing in capability upgrades, precisely because they see AI tools as multipliers of the kind of complex, judgment-intensive work that defines Level 3 service delivery.

The upskilling effort has taken concrete institutional form. Project UNLAD, a partnership between the industry, the Department of Information and Communications Technology, and TESDA, has already established 106 Enterprise-based Education and Training programs across 24 enterprises. The Skills Progression Partnership, developed with the Commission on Higher Education, is working to align university curricula with what the industry actually needs from graduates. A program called Byte the Gap has distributed over 1,641 laptops to the Department of Education, addressing digital access at the foundational level where the talent pipeline begins.

The ADB has been precise about what determines which countries capture the most from AI-driven productivity gains. In its April 2026 Asian Development Outlook, the institution stated:

“While generative AI has the potential to raise productivity and transform work, advanced economies are better positioned to benefit early due to stronger digital infrastructure, human capital, and innovation capacity. Many developing economies face binding constraints in computing capacity, skills, and data governance, which slow adoption and limit productivity gains. Catch-up in AI readiness can significantly improve growth outcomes, with services driving AI-enabled growth.”

The countries that close the AI readiness gap fastest will capture the largest share of the gains. The Philippines, through its coordinated upskilling infrastructure, is making a credible institutional bet that it can be one of them.

The Policy Foundation

Structural economic transformation does not happen in a regulatory vacuum, and the Philippine government has made two legislative moves that meaningfully improve the country’s competitive standing relative to its ASEAN peers.

The 99-Year Land Lease Law addresses a longstanding constraint on large-scale, long-horizon investment. By offering international developers and investors security of tenure comparable to what they can obtain in neighboring markets, the legislation removes one of the more persistent objections that has historically redirected regional real estate and infrastructure investment away from the Philippines.

The CREATE MORE Act, combined with clarified PEZA guidelines governing work-from-home arrangements, provides the kind of policy predictability that global firms require before committing substantial capital. Tax incentive clarity and ease-of-doing-business improvements may sound like bureaucratic achievements, but for companies evaluating multi-year operational commitments, they function as genuine risk-reduction mechanisms.

The IMF has been watching these policy moves closely. In its 2025 Article IV consultation on the Philippines, the Fund stated directly:

“Continued reforms to enhance investment and productivity are critical. Reforms can focus on addressing gaps in connectivity infrastructure, energy, and climate resilience, easing constraints on doing business, enhancing trade integration, tackling corruption, and strengthening governance and human capital. On the upside, accelerated implementation of structural and governance reforms can boost investment and FDI, increase fiscal multipliers and boost potential growth.”

The CREATE MORE Act and the 99-Year Land Lease Law address several of these points simultaneously, which is precisely why institutional observers have welcomed both measures as meaningful signals of reform intent rather than cosmetic policy adjustments. The World Bank reinforced this view, projecting that investment would strengthen as recent liberalization reforms in telecoms, transport, logistics, and renewable energy begin to improve the business environment for firms. Both institutions are, in effect, telling the same story: the policy direction is right, and the execution is what now matters.

The Inflation Complication

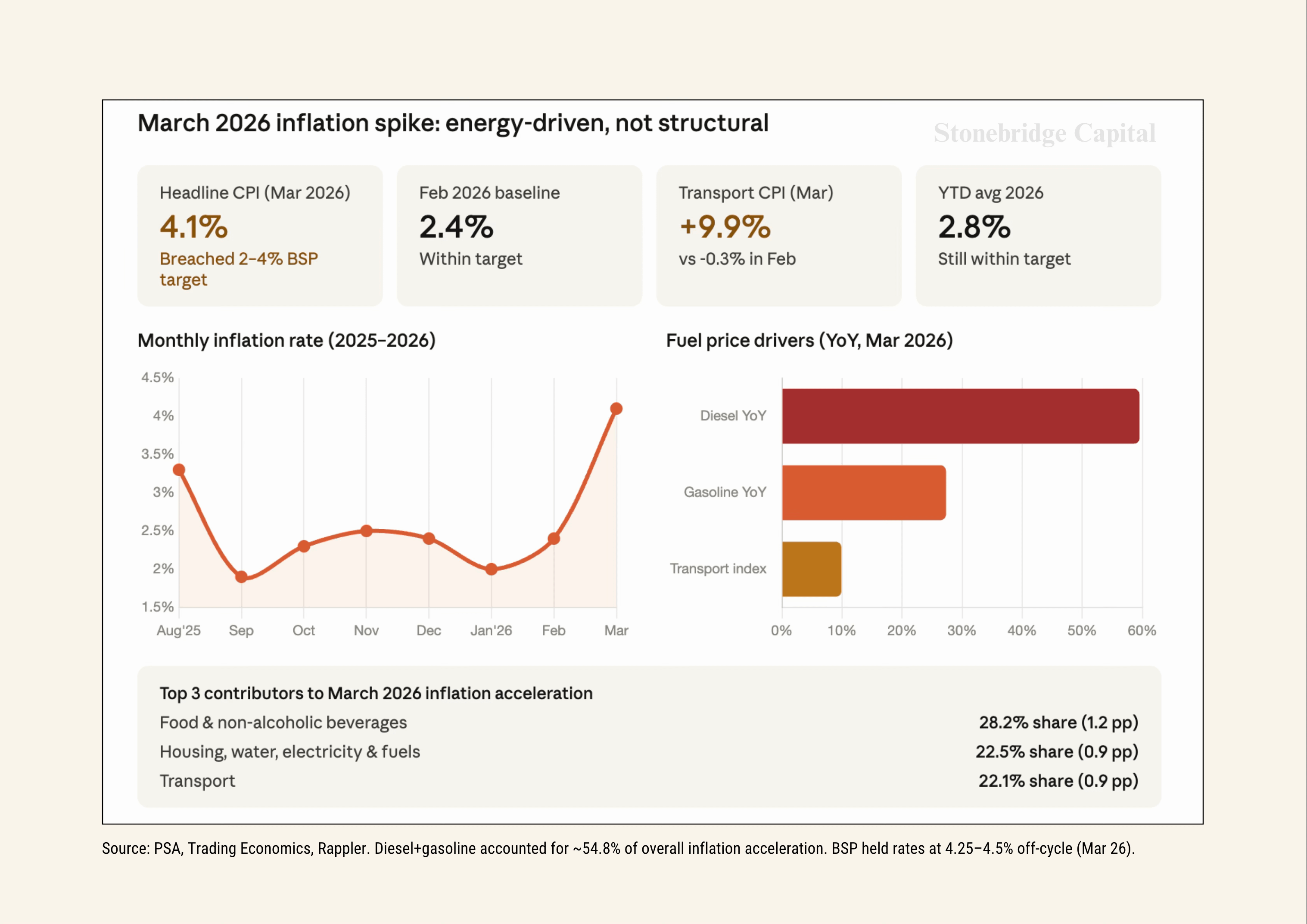

No honest assessment of the Philippine economy in 2026 can ignore what is happening to prices. Inflation reached 4.1% in March 2026, breaching the BSP’s 2% to 4% target ceiling. The primary driver was a 9.9% surge in transportation costs, itself largely a function of extraordinary fuel price movements: gasoline prices rose 27.3% year-on-year, while diesel surged 59.5%. These two items alone accounted for roughly 54.8% of the overall inflation acceleration, which means the inflationary episode is heavily concentrated in energy costs rather than being a broad-based price spiral.

The BSP responded with an off-cycle decision to hold policy rates at 4.5%, a cautious stance that reflects the central bank’s determination to prevent currency depreciation from feeding through into broader consumer prices. The ADB offered useful guidance on how governments across the region should navigate precisely this kind of energy-driven shock:

“Allowing higher energy prices to pass through, at least in part, can encourage energy conservation, fuel switching and investment in alternative energy sources. Fiscal support should be targeted and time-bound, with priority given to vulnerable households and heavily affected industries. Aggressive policy tightening could worsen growth pressures and heighten financial market volatility.”

This framing matters for the Philippines because it suggests the BSP’s decision to hold rates rather than hike aggressively is broadly consistent with the regional policy consensus on how to handle a commodity-driven inflationary shock. The OECD’s own reading of the inflation trajectory was similarly measured, noting that price pressures are expected to rise gradually toward the mid-point of the central bank’s target range as temporary effects from lower food and energy prices fade, with currency depreciation feeding into domestic prices only gradually as activity recovers. The inflation picture complicates the growth story without fundamentally altering it. Energy-driven price spikes are painful and politically sensitive, but they are also more tractable than structural inflation embedded across wages and services. The underlying economic architecture remains intact.

The Road Ahead

The Philippines has set a clear target for 2028: US$58.9 billion in annual IT-BPM revenue and 2.5 million direct jobs. The multilateral view on growth, while acknowledging near-term headwinds, remains constructive on the medium-term trajectory. The World Bank projects that growth will recover over the next two years, driven by strong domestic demand, with private consumption strengthening as inflation stays low and monetary easing lowers borrowing costs for businesses and households alike. The IMF, for its part, estimates that the Philippines may return to its growth potential of approximately 6% by 2028, which is precisely the horizon against which the IT-BPM sector’s Roadmap 2028 ambitions are calibrated.

The OECD, in its 2026 Economic Survey, offered what may be the most fitting summary of where the country stands:

“The Philippines has been among the world’s fastest-growing emerging market economies over the past decade and a half, despite several major shocks and a sharp COVID-related downturn. Output has more than doubled since 2010, while poverty has halved. Rapid growth in the working-age population, solid labour productivity gains and buoyant exports have underpinned this progress.”

The country’s position in 2026 can be summarized with reasonable confidence. It has a reserve buffer that provides genuine macroeconomic insulation. It has a bond market that has just earned a seat at the table of global index investors. It has a services sector in the early stages of a high-value transition that, if executed well, will sustain revenue growth through the automation era rather than being undone by it. It has legislative reforms that have removed some of the most durable obstacles to large-scale investment. And it has a demographic profile that continues to generate the kind of young, English-proficient labor force that global firms need at scale.

The risks are real. Inflation, currency weakness, and the execution risk inherent in any large-scale workforce transition are not trivial concerns. But the Philippines in 2026 is not a country in crisis. It is a country in the middle of a difficult and consequential transformation, one that is being managed with more institutional coherence than the peso chart alone would suggest.

For investors and observers tracking Southeast Asia, that is worth paying attention to.